Real Retirement Strategies (RRS): Using Extreme Growth for Income

- Subscribe to my YouTube Channel HERE.

When I first started to realize that income is the most important thing, my instinct was to, obviously, look at income-producing assets.

But as I started to dig much deeper, a weird question started to present itself.

Can extreme growth be used for income?

Growth is for ego. Growth for trying to look at green numbers in your trading account. Growth is for trying to sell things to people.

At least, that's what I thought.

Let's turn that around, though.

First, we need an instrument that shows massive growth. And since I track the highest growing ETFs (both leveraged and unleveraged) in the Dividend Income Program, all I had to do was go #1 on that real-time list.

The winner right now?

The VanEck Semiconductor ETF (SMH).

Even with its recent bearishness, it's been a monster.

While it's only been around since 2012, the growth is eye-popping.

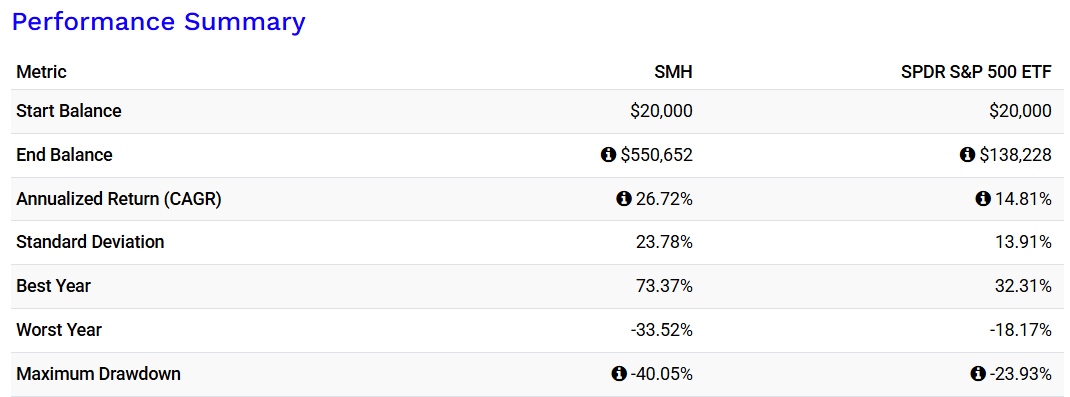

Here is the comparison between SMH and SPY from January 2012 to December 2025:

SMH has lapped SPY by a large margin.

What about the drawdown, though?

We'll get to that.

But for now, we have our extreme growth. How much can we pull out each year or each month?

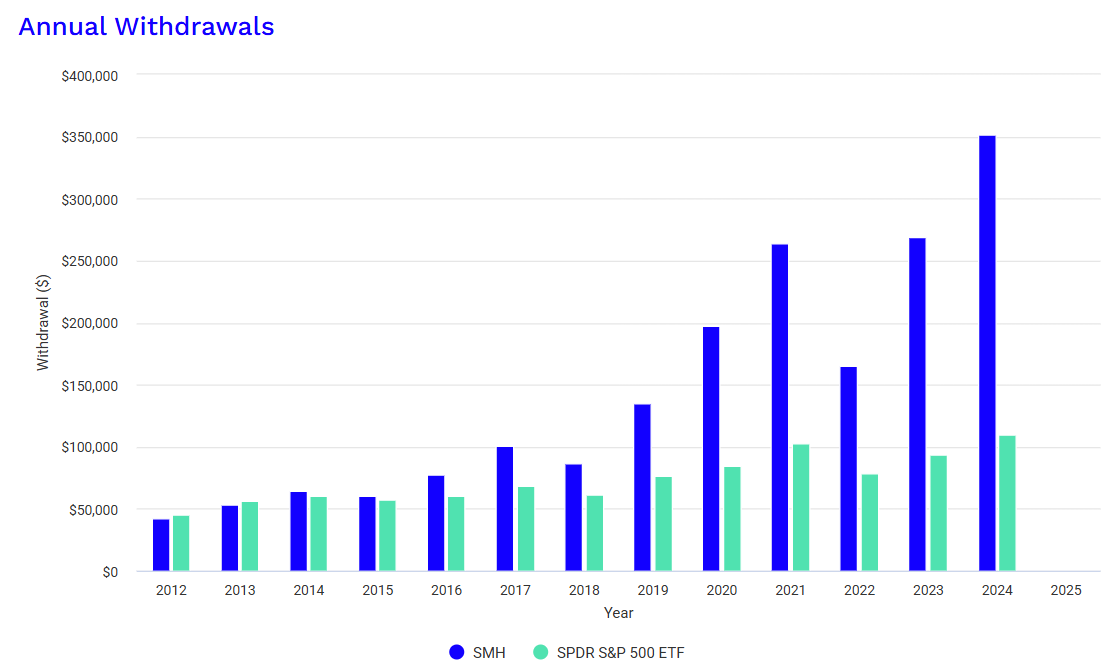

If we didn't add any money but started with $650,000, here's how we could do. Remember, our goal for all of these case studies is to be able to pull out $60k per year (or $5k per month).

Here are the Annual Withdrawals if we pull out 6% per year (a little above the sacred 4%):

We were short in 2012 and 2013, but by year 3 we could pull out $60k. And by 2025?

This year we'd probably be able to pull out over $350k.

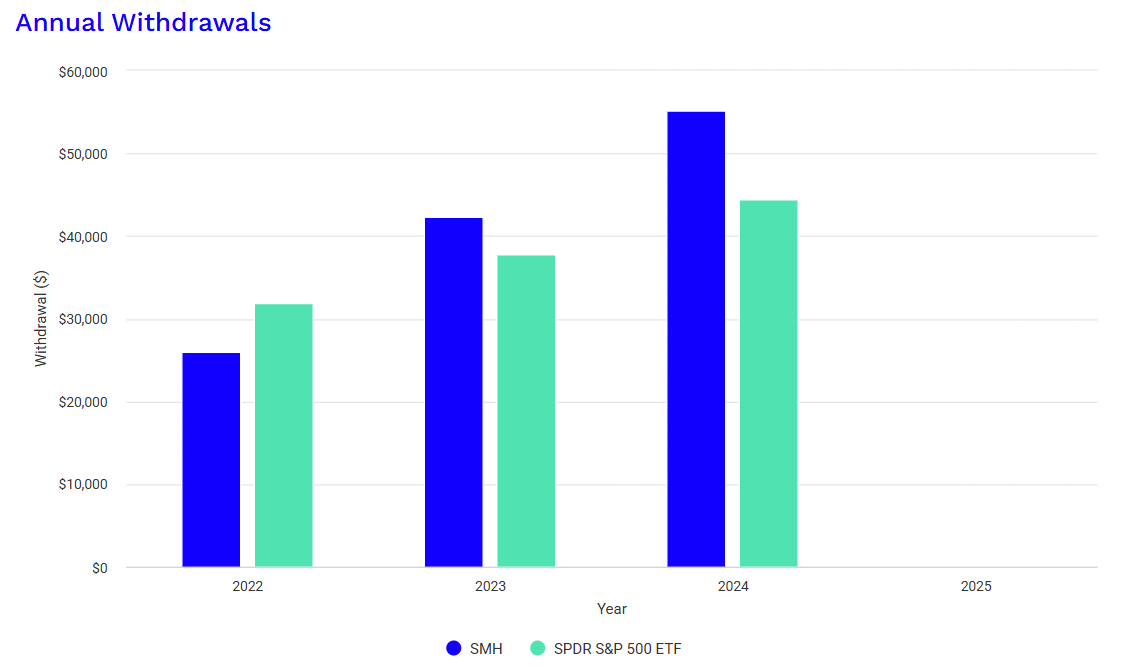

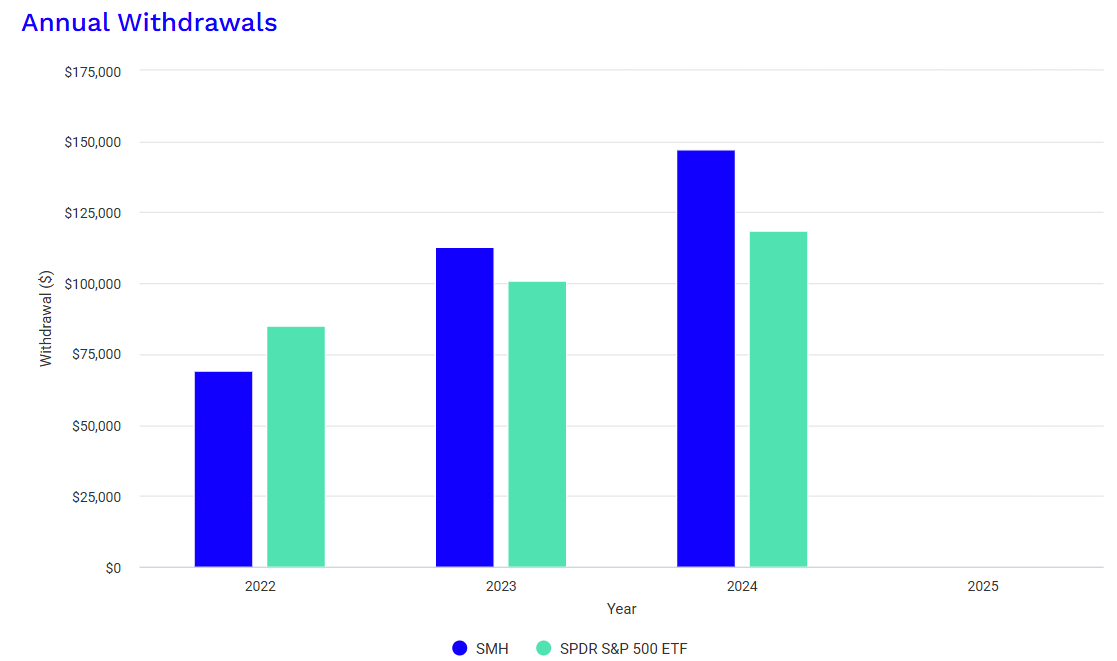

We still have the problem of that big drawdown. What if we started in 2022 at the beginning of that Bear Market?

If we started in 2022, we wouldn't have made it to our goal until the end of this year. That's the problem with drawdowns. They can hold you back when growth is the income engine.

Is there anything we can do?

Sure, we can add money each month until we get to our threshold. Then we can stop adding and let it ride from there.

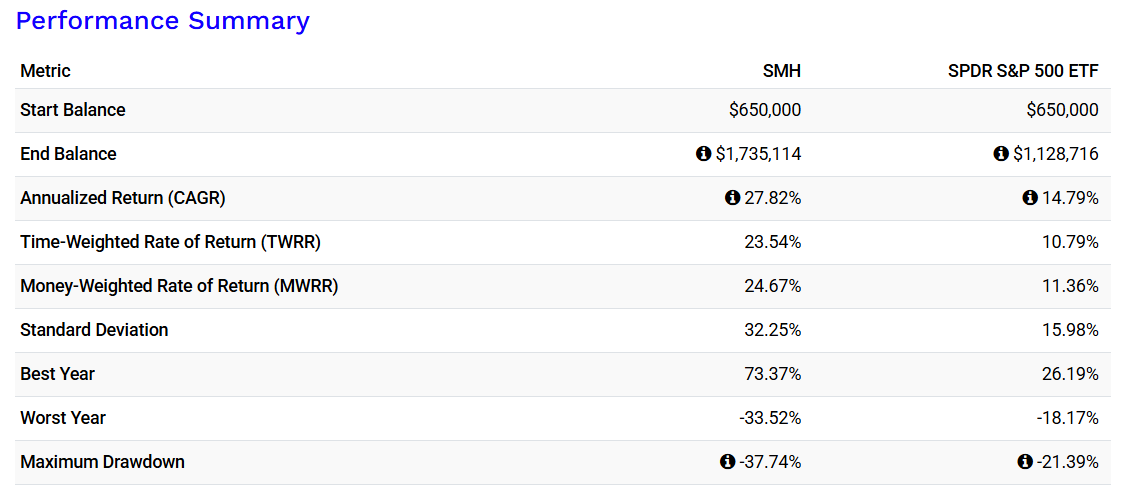

Here's what it looks like if we start in 2022 and add $2,000 each month to our original $650k:

In just three years, our nest egg has grown to $1.7 million. Now, if we start again in 2022 with $1.7 million and pull out 6%, what do we get then?

If we started with that higher amount, we'd be able to pull out $69k in year one and get as high as $147k by year three.

It would take three years, but that's not a long time to wait for possible financial independence.

Are there problems?

Yes. Everyone is calling for an AI Crash. If we get one, SMH will suffer horribly.

But so will everything else.

And is it hard to sell shares every year instead of just having the money flow in in the form of dividends?

Maybe.

But there's no denying the fact that extreme growth can definitely pay the bills.

Especially in bullish times.

We'll start looking at using dividends instead next.

Talk to you soon.

DISCLAIMER: This is not financial advice.

It should not be assumed that the methods, techniques, or indicators presented in these videos will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading. HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE UNDER- OR OVER-COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN.