Real Retirement Strategies: The Simplest Way to Independence

- Subscribe to my YouTube Channel HERE.

Every trader I've seen or met is focused on only one thing:

How much money can I make?

I was the same way.

Then, over two decades, I started to realize one very important thing.

It's not how much you make. It's how much you can actually take out.

For example, TQQQ makes more money than just about any other stock-related product.

And no one can retire on it. Why?

Because you can't take money out during bad years. A regular withdrawal would destroy any account if 2000 or 2008 happens again.

You say TQQQ makes a ton of money?

You can't safely take money out buying and holding TQQQ, so it's worthless.

And that's my focus now.

What can we use to take money out of our account safely...forever?

Because it's really the only thing that matters.

Today we'll look at the simplest way to retire, or more importantly, be financially independent.

It's the instrument that has the most data and is the instrument that's had the most books written about it.

The SPDR S&P 500 ETF Trust (SPY).

Yes, I've always hated index funds and the condescending people that promote them.

But being able to pull money out is what matters most. If SPY can do that, then it's worth consideration.

So, let's look at SPY from 2000-2025.

The goal for all of these investigations (this is the beginning of the Real Retirement Strategies series, or RRS) is to be able to pull out $5,000 per month, or $60,000 per year.

Some people might need more. Some might need less. But I want to try to help as many people as possible get to $5k per month. So I want to look at real solutions.

And I want to hear from anyone who can pull $5k per month out of their trading account -- regardless of the strategy they employ.

Please email me if you are!

For this very first case study, we'll use the mystical 4% rule.

We already know that if we take a set amount from SPY and that amount is too high, our account will go to zero. That's the whole motivation to look at income ETFs and stocks.

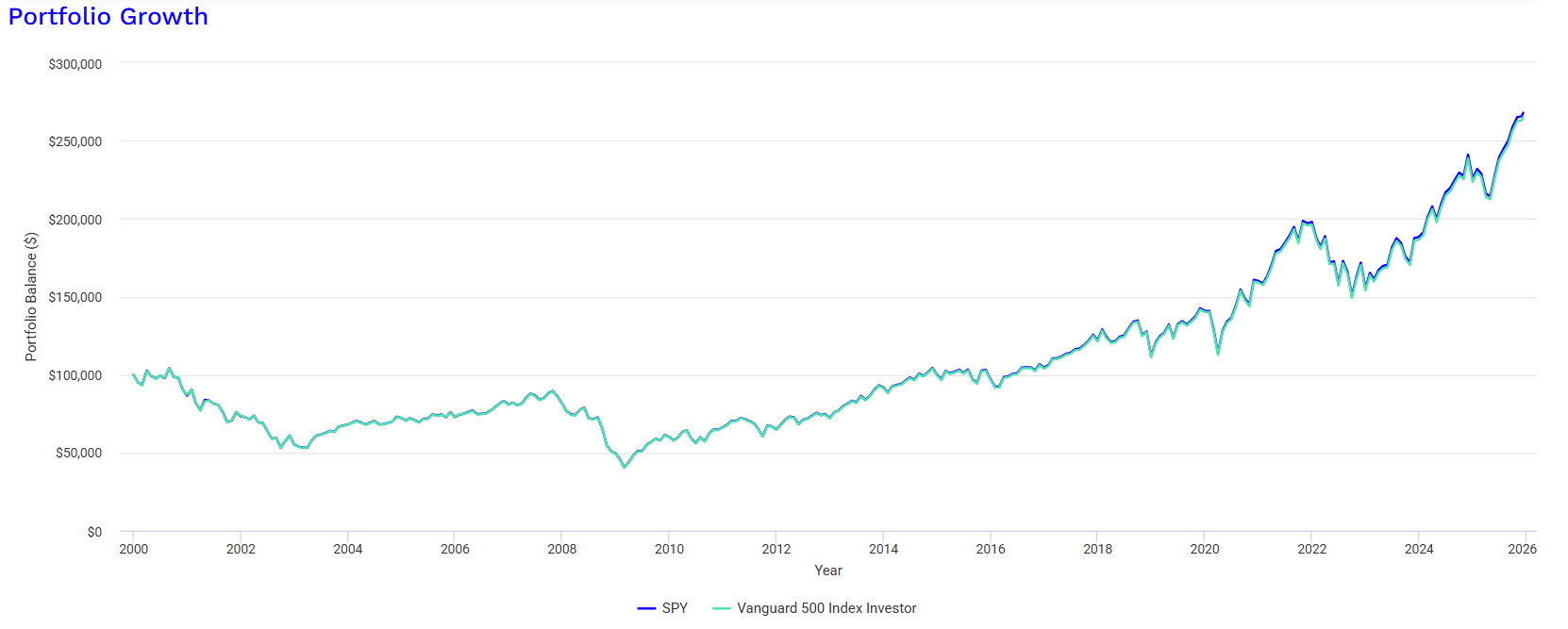

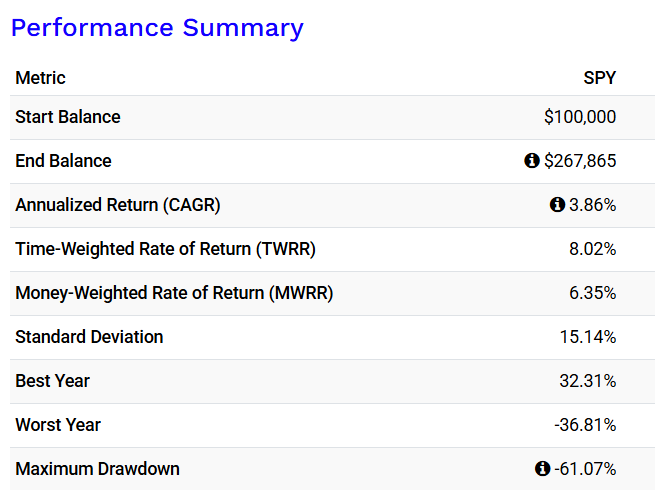

But can SPY survive if we just take 4% of our account balance each year? Here are the Reports on a $100,000 account from 2000-2025:

We would've gone through a massive drawdown...but we could've pulled out 4% per year from 2000 until now and still seen our account grow in the end.

But was that enough money to get to $5k per month or $60k per year?

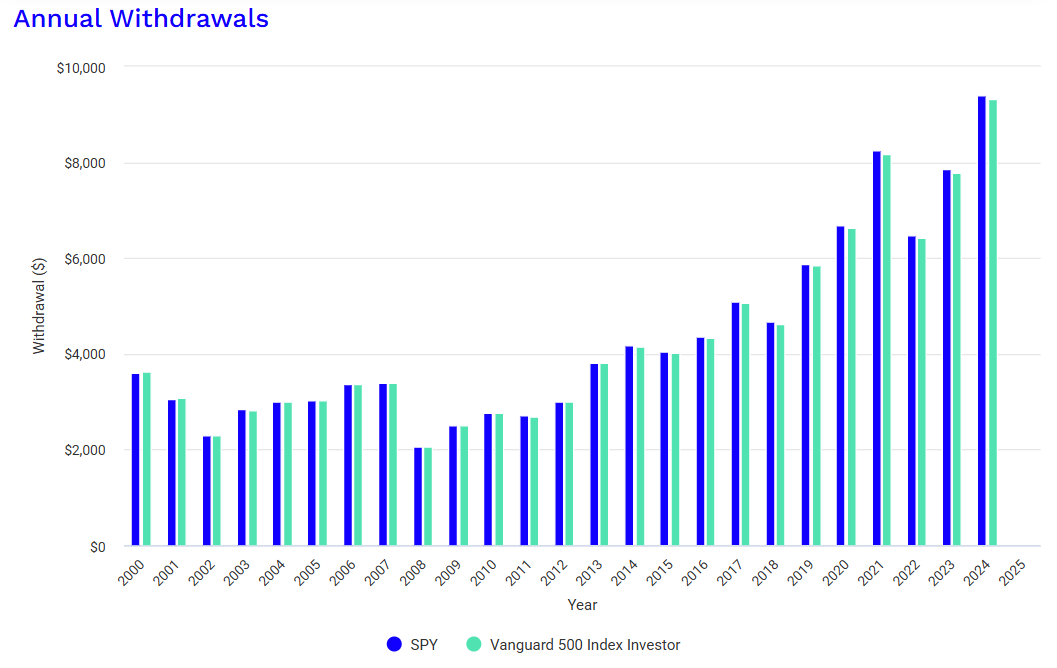

Here are the Annual Withdrawal amounts:

On just $100k, the most we ever could have pulled out in a year is $9,400. That's not going to cut it.

How much money do we have to have then?

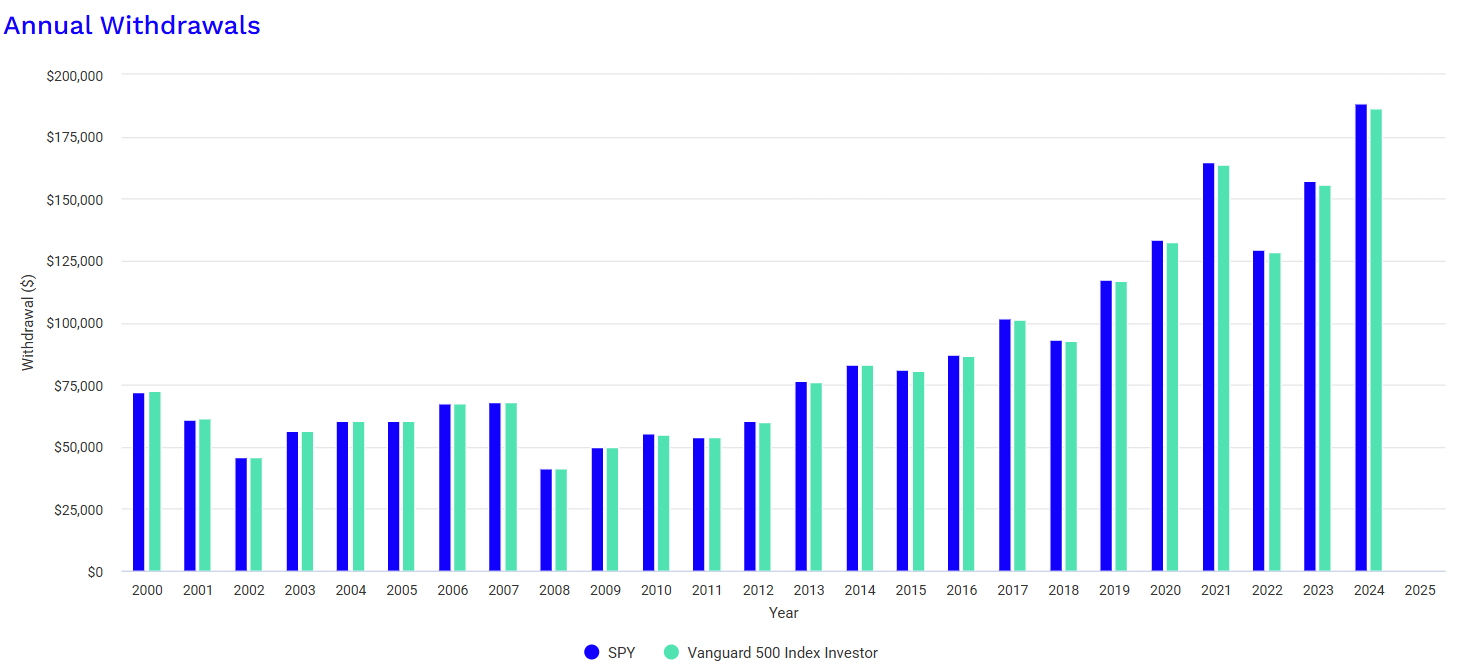

Here's the Report using a much larger account:

As you can see from the graph, the first two years of the Dot Com Bubble are actually fine. We're over $60k in both years.

But then we fall below by 2003.

However, we're back in business by 2004 and stay okay until the Financial Crisis of 2008-09.

In 2012, though, we are making our quota again and we've never looked back.

Last year we would've been able to take out over $188,000 -- and that's way over our $60k goal.

So, how big was our account to produce these numbers?

$2 million.

That's a lot. But it pretty much solves the puzzle.

It is scary during downturns and it has years where our payments wouldn't quite meet our needs, but it really pays off in the end.

We'd be living large by 2025.

Is it the best solution? Probably not. But it is a solution.

And that's going to be the focus of my trading life going forward.

Again, please email me with questions, comments, or different solutions. I want people to have real answers to the question, "When can I retire?"

Talk to you soon.

DISCLAIMER: This is not financial advice.

It should not be assumed that the methods, techniques, or indicators presented in these videos will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading. HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE UNDER- OR OVER-COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN.