The HUGE Danger of Selling Shares for Income

- Subscribe to my YouTube Channel HERE.

A famous college football coach once wisely gave his team an acronym to live by:

W.I.N.

What's Important Now?

And in the investing world, we never hear anyone talk about this.

We hear people get really worked up about how growth stocks are the only way to go, how high-yield is the new big thing, or how index funds are the only real solution.

We don't hear about how we're supposed to pay our mortgage next month.

Which actually is What's Important Now.

So let's look at how to get money each month.

The growth zealots and the index funders are adamant their way is the only way. After all, growth and index funding make money grow (sometimes). If we have more money, we have more money for retirement.

Therefore, we have money each month for our bills.

But do we, though?

Let's assume some small numbers. We'll just use a simple $10,000 account. (just add a zero or two to get to $100k or a million).

And we'll just pull out $100 each month from our $10,000 starting account. We're not going to use a percentage of our account because our mortgage doesn't change every month.

The mortgage is the mortgage.

So, what happens to our growth account if we sell shares to get $100 every thirty days?

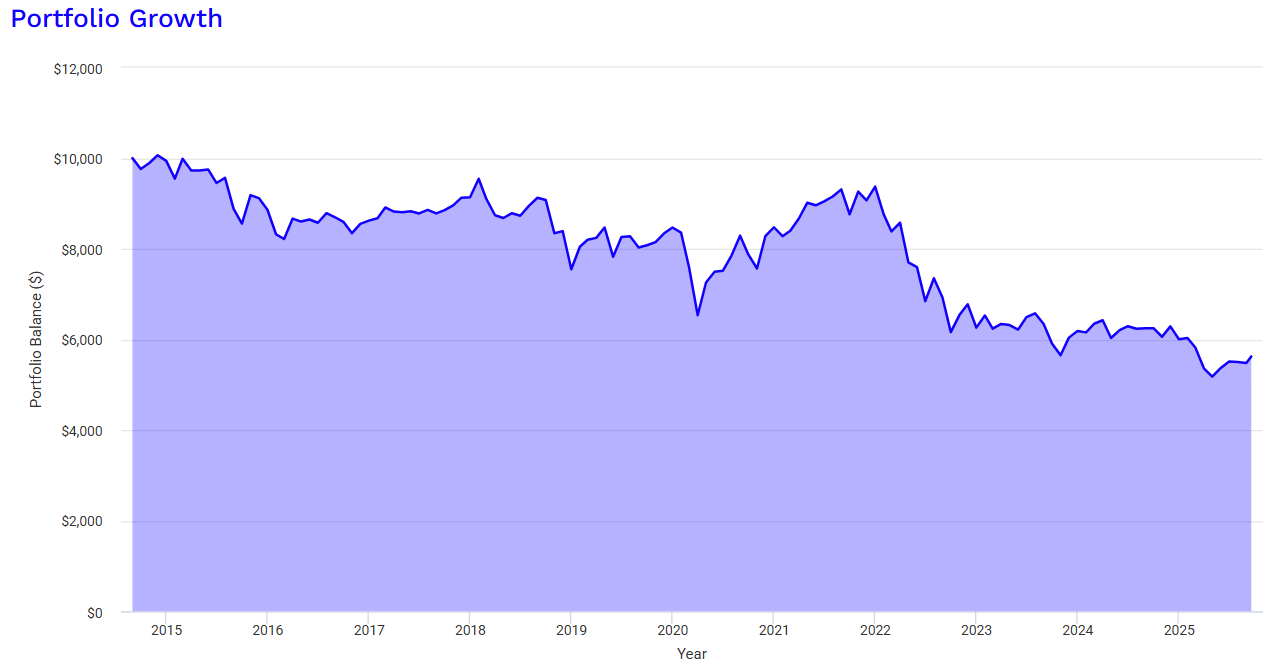

Here's that scenario on SPY since January 2014 (just over a decade). How did we do?

Oh no. We've gotten our $100 payment each month but now our account is in a death spiral. Our $10k is down to under $6k.

Our retirement account is on its way to zero--and there's no coming back. Imagine if this was a $1 million account. Buckle your seat belt, Dorothy. 'Cause our million dollar account is going bye-bye.

How do we know?

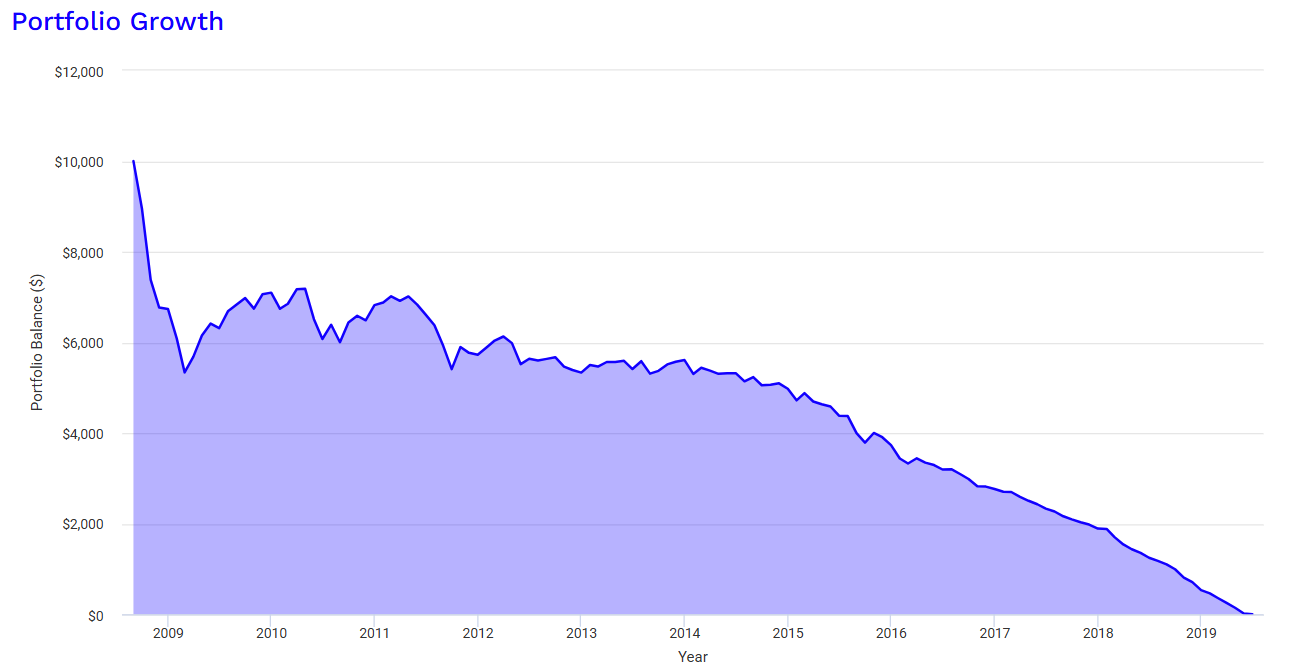

Because here's what happens if we take this scenario back to 2008:

All gone.

All-powerful growth has left us bankrupt.

The truly insidious part is that the death spiral may not come at first. And if we get lucky, it may not come for years.

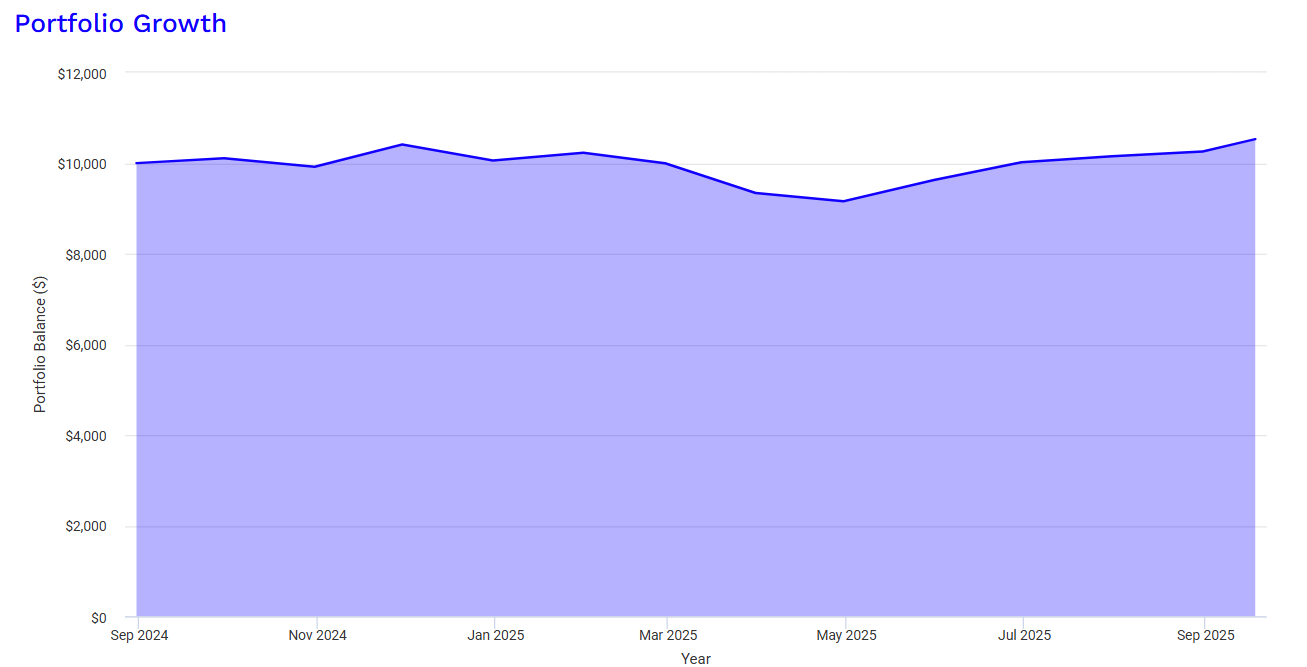

For example, here's the $100 per month withdrawal situation on SPY for the past year (September 2024 to September 2025):

It's not terrible in the past twelve months. SPY has increased a little.

But we know it's taken us to zero in the past. Will it do it again in the near future?

How do we ever trust selling shares for income again?

And is there anything we can do?

Here's one thing we can do: we can use an instrument that grows more than SPY. More growth means more money, and that additional performance can handle the $100 monthly withdrawal.

Right?

Here's SCHG and QQQ and SPY since September 2024. Both SCHG and QQQ have typically beaten SPY over time:

Well, look at that. Getting more growth has trounced SPY and given us our $100/month...and grown the account over the past year.

Mission accomplished?

Not so fast.

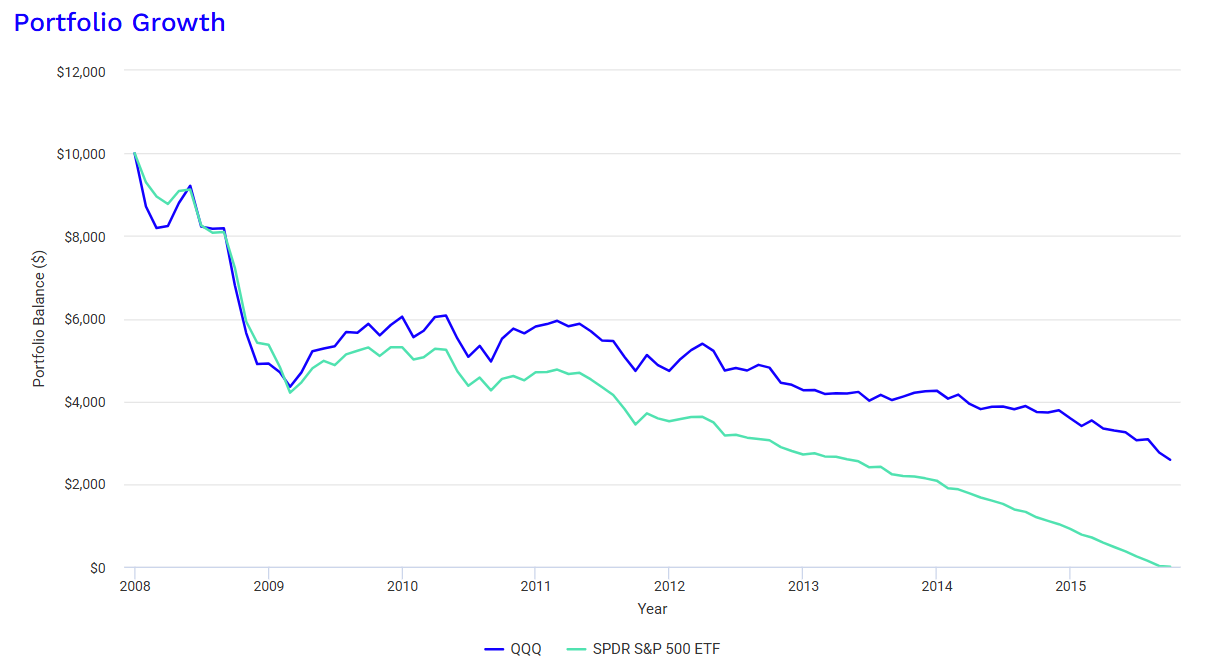

Here's what happens if we take QQQ back to 2008 (SCHG data doesn't go back that far):

We can see that SPY is a goner but QQQ does have a few thousand left. But we all know it's going zero like its growth-focused friend.

This is why selling shares for income is a very dangerous thing.

Now, growth advocates will scream, "You're taking out too much money! We can survive if we take out less!"

Okay, in many cases that's true.

But what if we don't want less money?

How can we get that $100, $1,000, or $10,000 a month if that's what we actually need right now?

High-yield/high-income ETFs.

The scourge of the growth world.

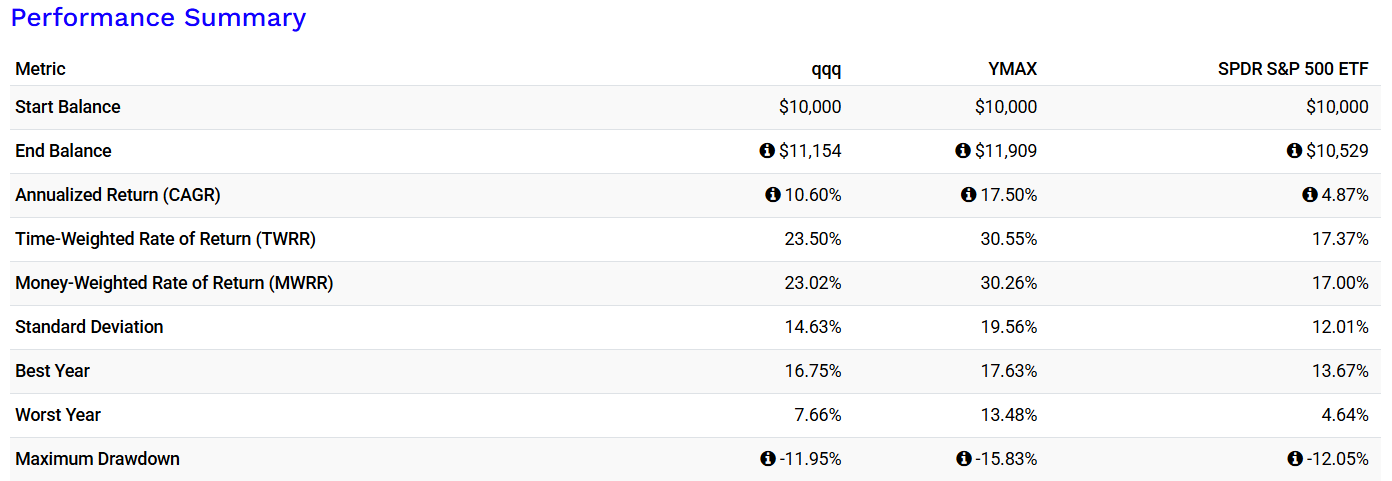

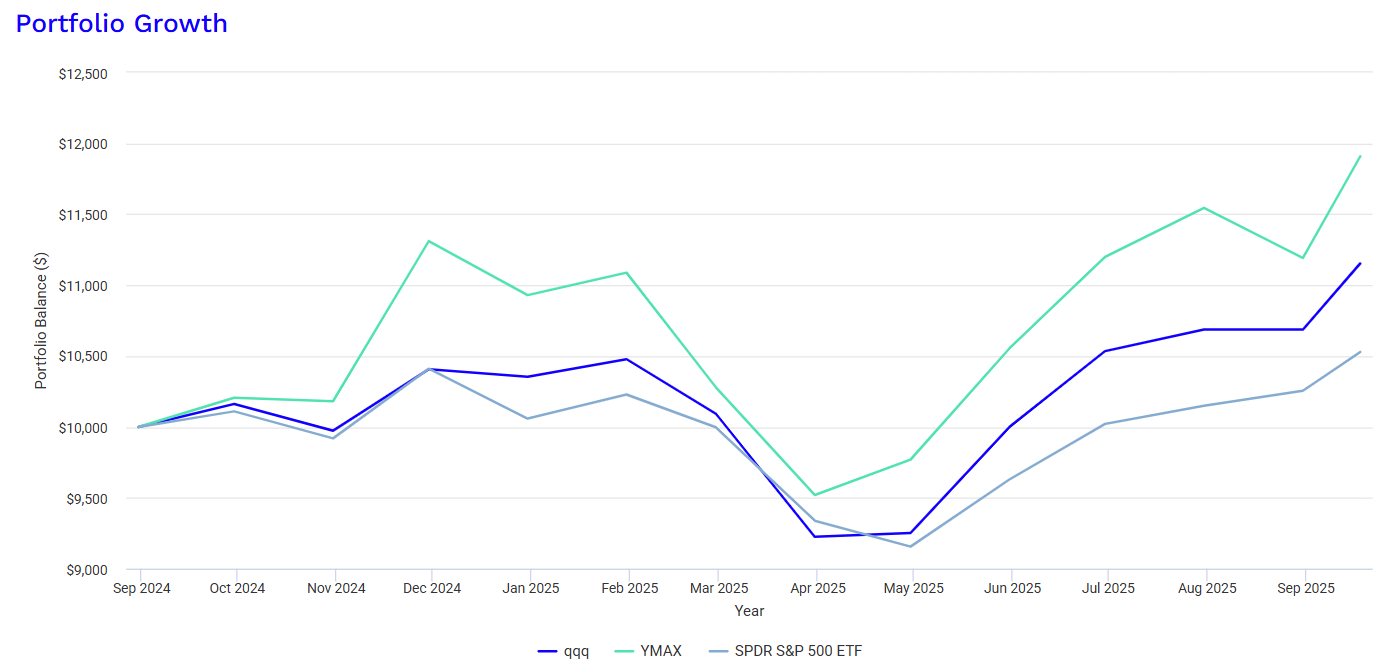

Here's the comparison if we use YMAX instead of growth in the past year:

Whoa.

By taking income from an instrument designed to give off income, we've gotten our regular payment AND seen our account grow a lot more than growth.

Here are the big questions:

- Will something that throws off way more income than is needed continue to stay stable or grow in the future?

- If we're reinvesting shares each month (due to surplus) and those extra shares also produce more income, will our income ever run out like it does for SPY and QQQ?

What do you think?

The facts show that an income ETF is far superior to selling shares to get the money we need now. At least, it has been in the past year.

The facts also show that selling shares to fund our financial future is a potential ticking time bomb. If we get the wrong market environment or we sell too many shares, we're toast.

So, people who want money each month are at a crucial crossroads: we can either lower our expectations -- or find a better way.

Talk to you soon.

DISCLAIMER: This is not financial advice.

It should not be assumed that the methods, techniques, or indicators presented in these videos will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading. HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE UNDER- OR OVER-COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN.