Are Growth ETFs Actually Good For Retirement?

- Subscribe to my YouTube Channel HERE.

It can be rough out there.

While YouTube is an incredible resource filled with people who are actually trying to help, there is a lot of garbage, too.

The problem is that some of that garbage seems like it might be true. And when it's delivered with confident smugness, it's easy to feel like we're dumb.

We see this the most when we start listening to growth zealots.

It's all about growth, bro. Income doesn't matter.

And I agree with that in part. Everyone likes more money.

Except the growth bros are embarrassingly short-sighted. Sure, a growth ETF will make a lot of money over time (hopefully), but no one answers the most important questions:

How much is enough? And how much can we pull out?

Growth dudes only focus on mine-is-bigger-than-yours. They never talk about what any of that actually means.

Here's an example.

Let's say my super-growth ETF portfolio is growing just like I hoped it would. Because I didn't waste my time on income, I've built up a nice nest egg of $500,000.

Woohoo, growth is the best!

Guess what?

You can't pull out more than 4% per year if you want to make sure you survive.

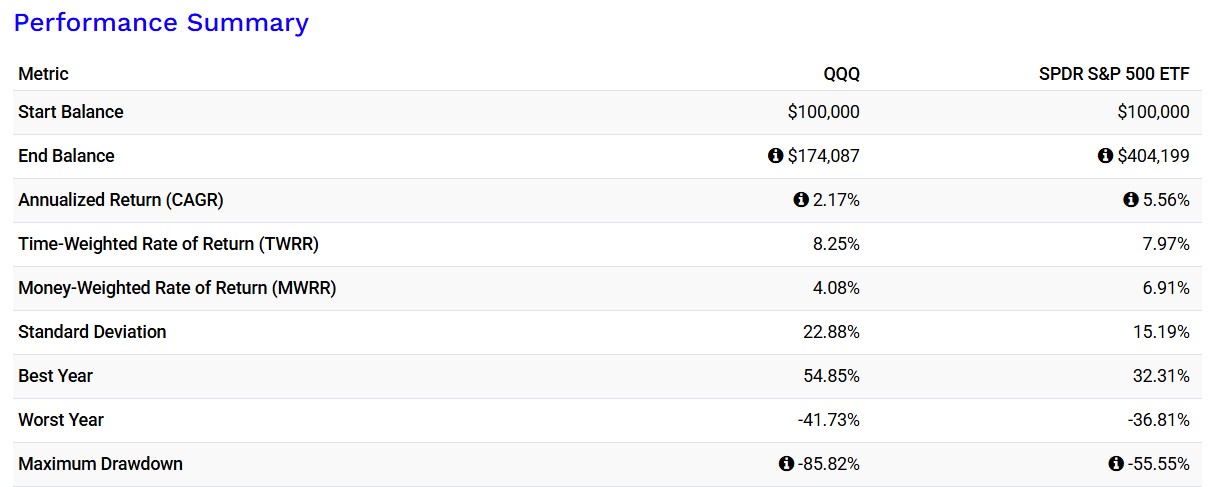

Here's QQQ since 2000 if we pull out 4% per year:

If we get another Dot-Com-like crash like everyone's talking about, we're in real trouble. Starting in 2000, a $100k portfolio that pulls out a mere $350 a month is gone by 2009.

Growth didn't save us.

Yes, we could hope that a crash like that doesn't happen again, and maybe we'll survive as we whistle past the graveyard.

Does anyone really want to take that chance?

Okay, then what's the survival number if we use growth? A paltry $150 per month.

Growth is underwater for years, only allows us to withdraw 1.8% of our balance annually, and badly underperforms SPY. But we survived!

Yikes.

Let's be bold, though. Let's say we can pull out a nice 3% per year.

Here's the big moment: how big does our dude-bro portfolio have to be if we want $5,000 a month in income and we pull out a safe 3%?

(waiting...)

Two million dollars.

Remember how our ballers cranked up their portfolios to $500,000 is just a handful of years?

Way to go...you're one-fourth of the way there.

That $500k means nothing if you want to retire tomorrow and need $5k per month.

But wait, what if $5k each month isn't realistic? What if we need $10k?

If that's the case, then we now need our account to grow to a whopping $4 million.

Now, just for fun, let's compare that to an income example.

I have a very close friend (and former tennis student) that is using income funds. He's not retired but he wants monthly income.

He has about $600k in his account.

How much did he make in September?

Using his Roundhill index-based portfolio divided into equal amounts and using actual distribution numbers from September, he made $17k last month.

Keep in mind, September was a low month because there were only 4 weeks and volatility was low. I've seen his returns and his usual month is much higher than that.

Nonetheless, if you made $17k per month, could you pull out $5k? Hmm.

And would you have to sell any shares like you would with growth?

Nope.

Last, consider this.

If my friend was a growth dude, his journey to retirement is only one-fourth completed. He still has a long way to go.

But in his current situation, he could theoretically retire tomorrow.

Right?

Which situation would you choose?

Talk to you soon.

DISCLAIMER: This is not financial advice.

It should not be assumed that the methods, techniques, or indicators presented in these videos will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading. HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE UNDER- OR OVER-COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN.